Is now the time for alternative valuation methods for the construction industry?

Who we areNews & publicationsOur publicationsSurveys and studies

Alternative Valuation Methods For Construction Ind

Whether it’s a local company or a major global entity, the valuation of a construction business is often estimated on the basis of multiples of earnings, and therefore essentially founded on a short-term outlook. However, businesses strategies with a long-term vision, such as innovation, energy, concessions and acquisitions are not taken fully into account in valuations. If valuers took a long-term view, through using other valuation methods that make it easier to understand these strategies, would this have an influence on how these firms are valued?

Our last study, How are major European construction groups performing?showed an average return of between 2.6% and 8.9% annually over the last ten years for our sample of 15 European groups.

This sector certainly presents its own particular risks, but it also has a number of attractions: a certain stability in the levels of results, average growth prospects of 4.1% annually until 2020, the impact of emerging countries with their keen demand for infrastructure, and a still-significant fragmentation in the sector (given that the 15 majors represent 12% of the European construction market), suggesting that there is scope for consolidation.

How far are these aspects taken into account by the market when valuing construction entities?

In additional to the analyses conducted for mergers and acquisitions and due diligence operations in this sector, we have talked to financial analysts and studied brokers’ reports on the listed values for our sample. The valuation of the concession business, which is based on specific business models, and of other activities (telephony, etc.) that are not connected with the construction industry have not been included in our analyses.

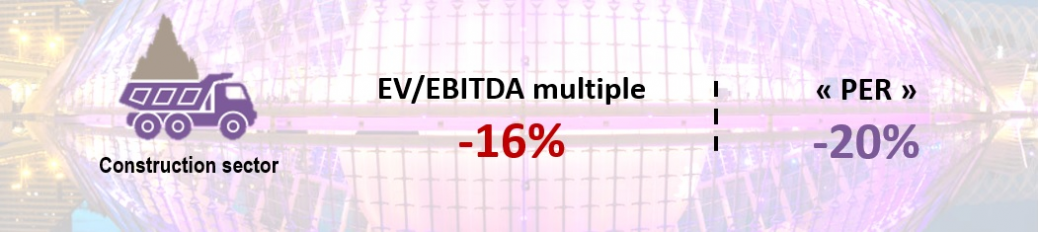

Only the market multiples method is used for valuations in the construction industry with market multiple levels below those in other sectors

Source : Aswath Damodaran

The levels of multiples for this activity remain lower than in other sectors. For the EBITDA multiple, the difference between the Engineering/Construction sector and the market average for all sectors is -16%. In the European zone alone, the valuation gap is similar, with a difference of -13% for the sample of 170 European Engineering/Construction entities.

For the Price Earnings Ratio (PER), we found a difference between the Engineering/Construction sector and the market average of -20%.

To find out more download our study below.

Want to know more?

Olivier Thireau Partner - Paris, France

2016 construction study

It is obvious that 2015 marked a slight recovery for our sample of major construction groups with an upturn in business and improved operating margins. Growth continues at both sectoral and geographic levels, with a boost in the energy and services sector and growth in business outside of Europe. However, companies are still affected by developments in their domestic markets, as can be seen in France,...